by Charlie Clarke

I have been frustrated with not being able to find economically interesting data on Japan, so I decided to fire up our Bloomberg terminal for the first time. It was amazing! Expect more data to come.

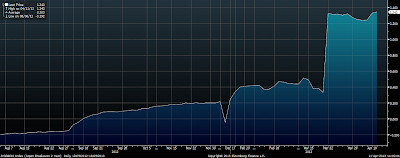

First, the five year Japanese breakeven rate:

Japan issues inflation indexed bonds, which means they pay real rates of returns. If inflation goes up, you get more money. They also issue regular nominal bonds that don't adjust for inflation. If you take the five year nominal bond minus the five year inflation indexed bond, you get a market estimate of expected inflation. Above is expected inflation over the last two years.

Looking at the graph, we see that inflation over the next five years is expected to be 1.43% right now. Also, The expected inflation rate has risen quite a bit over the year. In September of 2012, the Prime Minister Shinzo Abe was elected, the expected inflation rate has more than doubled since then. The BOJ didn't do anything until last week, but markets are forward looking.

On announcement last Thursday, the BOJ said that they intended to move to two percent inflation within two years. I wanted to see the time path of that change. Currently, the inflation in Japan (last reported Febuary) was -.6%. What is it expected to be over the next

year? Let's look at the 1 year break even rate:

*There are some risk premium issues in interpreting the breakeven rate as the market expectation for actual inflation, but it is a nice quick a dirty picture from the market.

P.S. - There is something interesting, in that if you compare the two year to the five year, you see that the five year is only 1.43%. So, inflation between year two in year 5 is expected to be about 1.5%. That is, it will be .35%, 2.3% then start falling average 1.5% those last 3 years. If the BOJ is serious and the market starts learning that over time, the five and ten year breakeven rates should rates should rise. Right now, the markets appear to be pricing in a substantial risk that the BOJ tightens eventually and misses their longer term target.

UPDATE: A commenter a Scott Sumner's blog points out that the Japanese market for inflation protected bonds is small and relatively illiquid. This is the "risk premium" problem I mentioned. If there is a liquidity premium on these bonds then the expected inflation rate is smaller than we estimated.

BE = IP - LIQ

IP = BE + LIQ

So the inflation rate, may actually be understated by the Japanese inflation protected bond market. On the other side of the coin, there may be an inflation risk premium. Maybe investors may want to be compensated in real terms more, in high inflation states of the world. That would push the other way.

More here.

I have been frustrated with not being able to find economically interesting data on Japan, so I decided to fire up our Bloomberg terminal for the first time. It was amazing! Expect more data to come.

First, the five year Japanese breakeven rate:

Japan issues inflation indexed bonds, which means they pay real rates of returns. If inflation goes up, you get more money. They also issue regular nominal bonds that don't adjust for inflation. If you take the five year nominal bond minus the five year inflation indexed bond, you get a market estimate of expected inflation. Above is expected inflation over the last two years.

Looking at the graph, we see that inflation over the next five years is expected to be 1.43% right now. Also, The expected inflation rate has risen quite a bit over the year. In September of 2012, the Prime Minister Shinzo Abe was elected, the expected inflation rate has more than doubled since then. The BOJ didn't do anything until last week, but markets are forward looking.

On announcement last Thursday, the BOJ said that they intended to move to two percent inflation within two years. I wanted to see the time path of that change. Currently, the inflation in Japan (last reported Febuary) was -.6%. What is it expected to be over the next

year? Let's look at the 1 year break even rate:

So over the next year inflation is expected to be .35%. So the market is not optimistic that inflation will pick up right away, nor did the BOJ say they were targeting that.

What about over two years?

Over the next two years, the market expects inflation to be 1.34%. So we can figure out the inflation expected next year with (.35 + I2)/2 = 1.34, which gives 2.33% [we could be more careful with geometric averages, but this will be very close with small inputs].

I'm struck by the rapid increase from .4% to 1.2% in the two year. This is the market rapidly adjusting up its estimate of when inflation will rise. The date March 19th is the date Kuroda took over the BOJ: "Haruhiko Kuroda took the helm at the Bank of Japan on March 19, vowing to do whatever necessary to break Japan's economy out of deflation and attain a 2 percent inflation target."

So, is Japan in a deflationary trap? Or do they have exactly the 2% inflation within two years they decided they wanted? The expected future path of inflation changed, before they even did anything.

*There are some risk premium issues in interpreting the breakeven rate as the market expectation for actual inflation, but it is a nice quick a dirty picture from the market.

P.S. - There is something interesting, in that if you compare the two year to the five year, you see that the five year is only 1.43%. So, inflation between year two in year 5 is expected to be about 1.5%. That is, it will be .35%, 2.3% then start falling average 1.5% those last 3 years. If the BOJ is serious and the market starts learning that over time, the five and ten year breakeven rates should rates should rise. Right now, the markets appear to be pricing in a substantial risk that the BOJ tightens eventually and misses their longer term target.

UPDATE: A commenter a Scott Sumner's blog points out that the Japanese market for inflation protected bonds is small and relatively illiquid. This is the "risk premium" problem I mentioned. If there is a liquidity premium on these bonds then the expected inflation rate is smaller than we estimated.

BE = IP - LIQ

IP = BE + LIQ

So the inflation rate, may actually be understated by the Japanese inflation protected bond market. On the other side of the coin, there may be an inflation risk premium. Maybe investors may want to be compensated in real terms more, in high inflation states of the world. That would push the other way.

More here.

No comments:

Post a Comment